Stablecoin Yield Explained: Why Stablecoin Interest Rates Are Higher Than Traditional Banks

Elena Beech

Key Takeaways

Stablecoin interest rates are higher than traditional banks because stablecoin yield products pass more of the underlying return directly to users, rather than capturing it as net interest margin.

Stablecoin yield is the return you earn by depositing stablecoins into third-party lending protocols, liquidity pools, or centralized finance platforms. In 2026, stablecoin interest rates at institutional-grade platforms range from approximately 0.5% to 33.95% APR, which is well above what most banks offer on USD deposits. Traditional USD bank deposits typically pay around 0.38% to 2.8% APY, while some higher-yield USD accounts can reach about 4% APY.

For fintech executives and neobank CFOs asking why, the answer lies in the market structure: banks capture the spread between what they earn on assets and what they pay depositors, while stablecoin yield infrastructure is designed to pass more of that return directly onto the holders.

This article explains what stablecoin yield is, where it comes from, whether high stablecoin yields are sustainable, and what warning signs to watch for.

Disclaimer: All yield figures cited are variable and based on prevailing market conditions. Past performance is not indicative of future results.

What Is Stablecoin Yield?

A stablecoin is a digital asset pegged to a fiat currency, most often the U.S. dollar.

The token itself does not appreciate in price; the yield is generated separately by deploying the reserves backing those tokens into income-producing activities.

When a user holds a stablecoin in a yield-bearing product, the issuer or platform utilizes the underlying dollar value by investing it in different ways, such as buying government bills, lending it to borrowers, executing arbitrage strategies, or using DeFi strategies. Yield products each carry different risk profiles, allowing customers to select a strategy that matches their risk appetite and optimize for their preferred risk-adjusted returns.

A portion of the income from those activities is then returned to holders, either as a rebasing token, an accruing wrapper, or a direct interest payment.

Why Are Stablecoin Yields Higher Than Traditional Bank Savings Rates?

Banks use the money received from deposits to invest in loans, government securities, and other assets. In the United States, the federal funds rate has held around 3.75% in early 2026. When a bank earns that rate on its deposits, it may give depositors 0.5% or less and keep the difference as its net interest margin. That spread funds their operations, regulatory capital requirements, and profit.

The U.S. GENIUS Act is designed to require major fiat-backed stablecoin issuers to keep reserves on a 1:1 basis, meaning that each stablecoin in circulation is backed by an equal amount of assets.

The stablecoins themselves typically do not pay yield directly. Instead, yield is generated through separate infrastructure layers such as tokenized treasury products, lending strategies, or on-chain vaults that pass through a larger portion of the underlying returns to users.

Because stablecoin infrastructure is software-native and globally accessible, distribution costs are significantly lower than those of traditional financial institutions. This allows fintechs and digital asset platforms to offer users higher dollar-denominated yields for treasury-backed products and even higher yields for DeFi-based strategies with some additional risk.

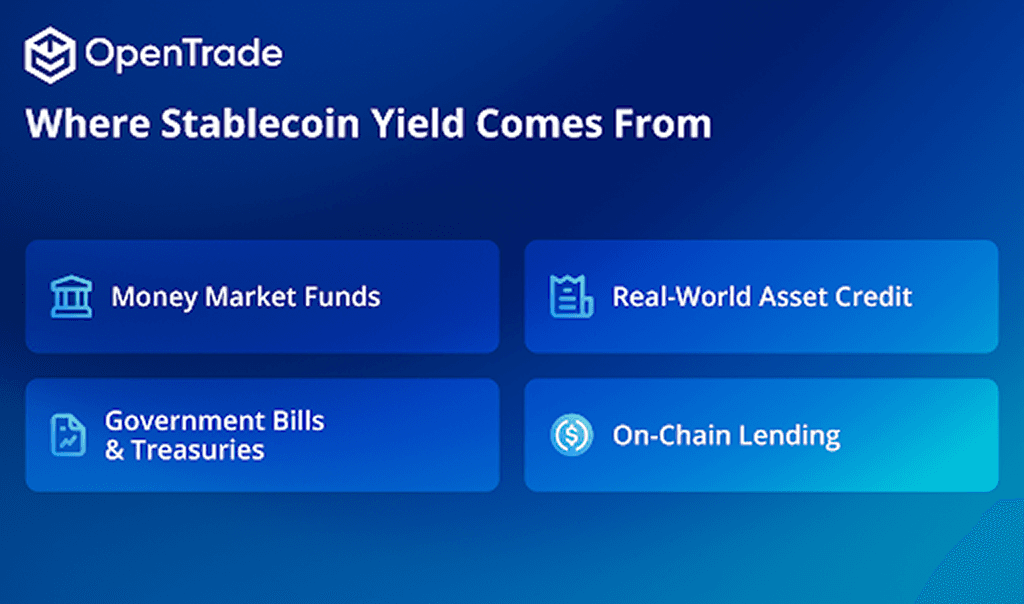

Where Do High Stablecoin Yields Actually Come From?

There are five primary yield engines in the stablecoin market. Each has a distinct risk profile.

1. Government bills and money market funds

These are one of the lowest-risk yield sources. The issuer holds short-duration U.S. Treasuries or invests in money market funds backed by government securities, then passes the yield to holders. In Q1 2026, tokenized T-bill products were generating approximately 4% to 4.8% APY. Both asset types are backed by the faith and credit of the U.S. government, which makes them the closest thing to a risk-free return available in traditional finance.

2. On-chain lending

Stablecoins are lent to borrowers who post collateral exceeding the loan value. Borrowers pay an interest rate that rises and falls with demand. In 2026, lending rates on major DeFi protocols have ranged from 4% to 12% APY, depending on utilization and market conditions.

3. Basis and funding trades

Some protocols pair stablecoin reserves with short positions in perpetual futures, capturing the spread between spot and futures prices. This strategy typically generates above-market yields when funding rates are positive but compresses significantly when market conditions shift.

4. Real-world asset credit

Stablecoin reserves are deployed into off-chain credit structures: trade finance, private credit, and commercial paper. Returns are higher than pure T-bill strategies because the underlying loans carry credit risk. This engine requires robust due diligence on the underlying borrowers, origination standards, and legal protections around the capital.

5. Staking-based returns

Some blockchain networks pay rewards to participants who help validate transactions, a process called staking. These rewards are paid in the network's native token, such as SOL for the Solana network, which means the value of those rewards can go up or down with the token's price.

Some yield products capture those staking rewards while simultaneously taking an offsetting position that cancels out the price exposure. The result is that the holder receives the staking income without taking on the volatility of holding the underlying token.

OpenTrade's Stablecoin Staking Yield, powered by Figment, uses this mechanism.

Are High Stablecoin Yields Sustainable?

Sustainable yield is yield that can be traced directly to economic activity. T-bill yield is sustainable as long as the risk-free rate remains above zero. Lending yield is sustainable as long as there are borrowers willing to pay for leverage. Real-world assets (RWA) credit yield is sustainable as long as the underlying borrowers service their debt.

The relevant question for any yield product is not whether the headline rate is high, but whether the source of that yield is identifiable, verifiable, and proportionate to the rate offered.

This distinction is especially important in digital assets, where some protocols have historically relied on token emissions or unsustainable incentives to artificially boost returns. While these mechanisms can temporarily increase yields, they are often dependent on continued subsidy rather than underlying cash flow generation.

Institutional stablecoin yield products are increasingly shifting toward more sustainable models backed by short-duration U.S. Treasuries, private credit, overcollateralized lending, or other income-generating assets with measurable returns.

That said, stablecoin interest rates are sensitive to macroeconomic conditions. For example, if the U.S. Federal Reserve cuts rates significantly, T-bill-linked products will see their yields compress. Products that combine multiple different yield sources tend to offer more stable rates than those relying on a single yield source.

Warning Signs of Unsustainable Stablecoin Yield

Not all high stablecoin yields are credible or safe. The following are specific indicators of structural risk.

Unclear yield source

If a platform does not publish what generates its yield, that is a primary risk indicator. Reputable products publish reserve composition, underlying assets, and yield attribution.

Excessive leverage

Some platforms amplify yield by taking leveraged positions. Leverage increases return in favorable conditions but can trigger rapid losses when markets move against the position. Basis trade products are particularly susceptible to this during periods of negative funding rates.

Token emissions

A common pattern in DeFi is offering high "yield" that is funded by issuing the platform's own governance token rather than by genuine economic return. This inflates the advertised APY without generating real value. When token emissions stop or the token price falls, the yield disappears. This is not yield; it is inflation of a token with no guaranteed value.

Unrealistic APYs

In the current rate environment, APR above approximately 10% to 12% on a USD-denominated product warrants detailed investigation. Returns in that range are achievable through higher-risk credit strategies or basis trades, but they carry corresponding risk. Double-digit yields from unspecified sources should be treated as a warning sign.

5. Poor transparency

Transparency is not optional for institutional-grade yield products. The standard in 2026 includes published reserve composition, independent attestations, and real-time reporting accessible to holders.

SIERRA, the Liquid Yield Token built on OpenTrade's infrastructure, publishes its full reserve composition, live NAV, and yield source breakdown in real time at app.sierra.money/transparency, with weekly attestations from an FCA-regulated asset manager. That is the level of disclosure to look for in any yield product.

Understanding where stablecoin yield actually comes from makes it easier to evaluate which products are suitable to you. The yield sources delivering returns in 2026 are diverse: U.S. Treasury income, bonds, private credit, lending demand, trade finance, staking rewards, and more.

Each carries a different risk profile, and understanding the differences is what separates a credible yield product from a risky or unsustainable one. Learn more about which yield products OpenTrade offers here.

The key consideration to keep in mind for any yield product is not to get the highest possible rate, but whether you can identify what generates it and whether that source is proportionate to the return being offered.

For fintechs and neobanks looking to offer stablecoin yield to their users, or put their own stablecoin balances to work, get in touch at opentrade.io/contact.

What are the five biggest stablecoins?

By market capitalization as of early 2026, the five largest stablecoins are Tether (USDT) at approximately $185 billion, Circle's USDC at approximately $75 billion, Sky's USDS, Ethena's USDe, and PayPal's PYUSD. USDT and USDC together account for the large majority of the total stablecoin supply.

How do stablecoin yields differ from traditional interest or staking returns?

Traditional bank interest is paid by the bank from its net interest margin, which represents the difference between what the bank earns on its assets and what it pays depositors. Stablecoin yield products, by contrast, pass through returns from specific identifiable assets. Staking, in the blockchain context, refers to locking tokens to secure a proof-of-stake network in exchange for block rewards. Stablecoins do not stake because they do not secure a network. Products marketed as "stablecoin staking" are typically depositing user funds into a yield wrapper or lending market, and should be evaluated on those terms.

What are the main risk factors that affect stablecoin returns?

The primary risk factors include: interest rate risk, where returns linked to the risk-free rate compress when central bank rates fall; credit risk, where returns from lending or RWA products depend on borrower performance; smart contract risk in DeFi-based products; basis risk in funding-rate strategies; counterparty risk when capital passes through intermediaries; and liquidity risk if the product does not allow timely redemption. The appropriate response is to understand which risks apply to a given product before deploying capital, not to avoid stablecoin yield altogether.

For information on how OpenTrade enables fintechs and neobanks to offer stablecoin yield products, visit opentrade.io/contact.

All yields referenced in this article are variable. Past performance is not indicative of future results. This article is for informational purposes only and does not constitute financial advice.

Elena Beech