The Future of Stablecoin FX Markets in LATAM

Elena Beech

Key Takeaways

Stablecoin FX (Foreign Exchange) markets refer to the digital ecosystem where different national currencies are traded against each other using blockchain-based stablecoins rather than traditional banking systems.

Cross-border payments in LATAM have always been expensive. Moving money between countries means routing through a chain of traditional banks, each of which is taking a cut.

For example, sending $200 USD from Brazil to Bolivia can cost up to $103.52. Settlement typically takes between 2 and 5 business days, but can be longer. For a worker waiting on that money to cover rent or groceries, five days is a long time to wait.

Stablecoin FX markets replace that chain entirely. Money can move directly between wallets, settling in seconds, 24/7. In fact, 71% of LATAM institutions already use stablecoins for cross-border payments, the highest adoption rate globally.

This article covers how stablecoin FX corridors work, which platforms are building on them, and what it means for companies operating across the region.

Why Stablecoin FX Markets Are Taking Off in LATAM

The economic landscape across LATAM created the ideal conditions for stablecoins to take off. The average inflation across the region for 2026 is 17.47%, with Venezuela being the highest at 220%. Venezuela has seen inflation rates that made local savings effectively worthless within months.

Currency devaluation and capital controls are chronic features of the financial landscape in LATAM, and they create persistent demand for dollar-denominated savings and payment options that local banking infrastructure has never been able to meet at scale.

Traditional banking was designed for a different era and a different set of problems. Moving money from Mexico to Colombia, or from Brazil to the U.S., passes through a chain of intermediary banks, each with its own fee schedule and its own settlement window.

Onchain FX is the model that changes this. Using smart contracts to execute asset swaps 24/7 without traditional correspondent banks, on-chain FX gives exchanges and fintechs a settlement layer that operates on internet time rather than banking hours.

Why Traditional LATAM Cross-Border Rails Are Failing Exchanges

For exchanges running high-volume cross-border B2B payment operations across LATAM, traditional rails create structural cost across four specific areas.

The T+3 settlement problem. Payment authorization happens instantly, but the actual fund transfer does not. Banks settle in batches, during business hours, on working days, which means capital is in transit for 2 to 5 days, sometimes more if there are holidays. This means cash is unavailable for redeployment or reinvestment during that time. For an exchange processing thousands of transactions per day across multiple corridors, that settlement lag represents a significant amount of locked working capital.

Correspondent banking fees at every hop. A payment from Colombia to Brazil moves through a chain of correspondent banks, each with its own fee schedule and spread. According to EY's 2025 stablecoin survey, 41% of current stablecoin users in B2B cross-border payments report cost savings of at least 10%, with mid-size firms reporting savings of 10-20%. The spread between what a business pays to initiate a transfer and what arrives at the destination is rarely transparent until after the fact.

Pre-funded nostro accounts. To process same-day payments across currency pairs, institutions must maintain pre-funded accounts in each market they operate in. For every corridor an exchange wants to serve, capital sits idle in a pre-funded account, generating no return.

FX spread opacity. Traditional FX pricing on crypto remittance corridors is structured to hide the real cost. The spread between buy and sell rates is baked into the quoted rate, not disclosed separately. For exchanges processing significant volume, even a 0.5% improvement in FX transparency compounds meaningfully at scale.

As Rodrigo Faria from Bitso put it in OpenTrade's Stablecoin Surge report: "Moving money should be like roaming with your phone. You travel abroad, and your phone just works, and the telecom companies handle everything behind the scenes." That is what stablecoin FX infrastructure is building toward, and the exchanges that have moved earliest are already seeing it in their numbers.

How Stablecoin-Enhanced FX Corridors Work

Here is exactly how a corporate payment moves through a stablecoin FX corridor in practice, using the US-Mexico corridor as an example.

Step 1: Local Fiat On-Ramp

The business sending the payment first converts local currency into a USD-denominated stablecoin using the standard local banking system. Instead of routing this money through a slow network of international intermediary banks, the payment provider instantly converts the cash into a USD-backed digital stablecoin. This happens entirely within the provider's own secure infrastructure at a transparent, real-time exchange rate.

Step 2: On-chain Transfer

The stablecoin moves on-chain from the sender's wallet to the recipient's wallet in seconds, 24/7, including weekends and public holidays. Transaction cost is typically below $0.10 regardless of the transfer amount, compared to $15-100 for a traditional international wire, according to McKinsey's Global Payments Report 2025. Bitso processed over $6.5B in US-Mexico remittances in 2024 on this model, serving 1,900+ enterprise clients, each moving money through corridors where correspondent banking had traditionally made settlement slow and expensive.

Step 3: Local Off-Ramp Settlement

At the destination, the receiving exchange or payment provider converts the stablecoin back to local currency and deposits it into the recipient's local account. The recipient receives local currency in their account, and from their perspective, the transaction looks and feels like any other domestic transfer.

For exchanges using OpenTrade's yield infrastructure, idle stablecoin balances accumulated between steps two and three can earn institutional-grade yield rather than sitting uninvested. belo, the cross-border payments app operating across 17 countries in LATAM.

OpenTrade's infrastructure enables clients to earn returns on its stablecoin treasury rather than holding idle balances. belo has over 3 million users in 17 countries and is the #1 app for cross-border payments in LATAM. belo used OpenTrade to offer 4% APR on USDT and USDC balances directly within their app.

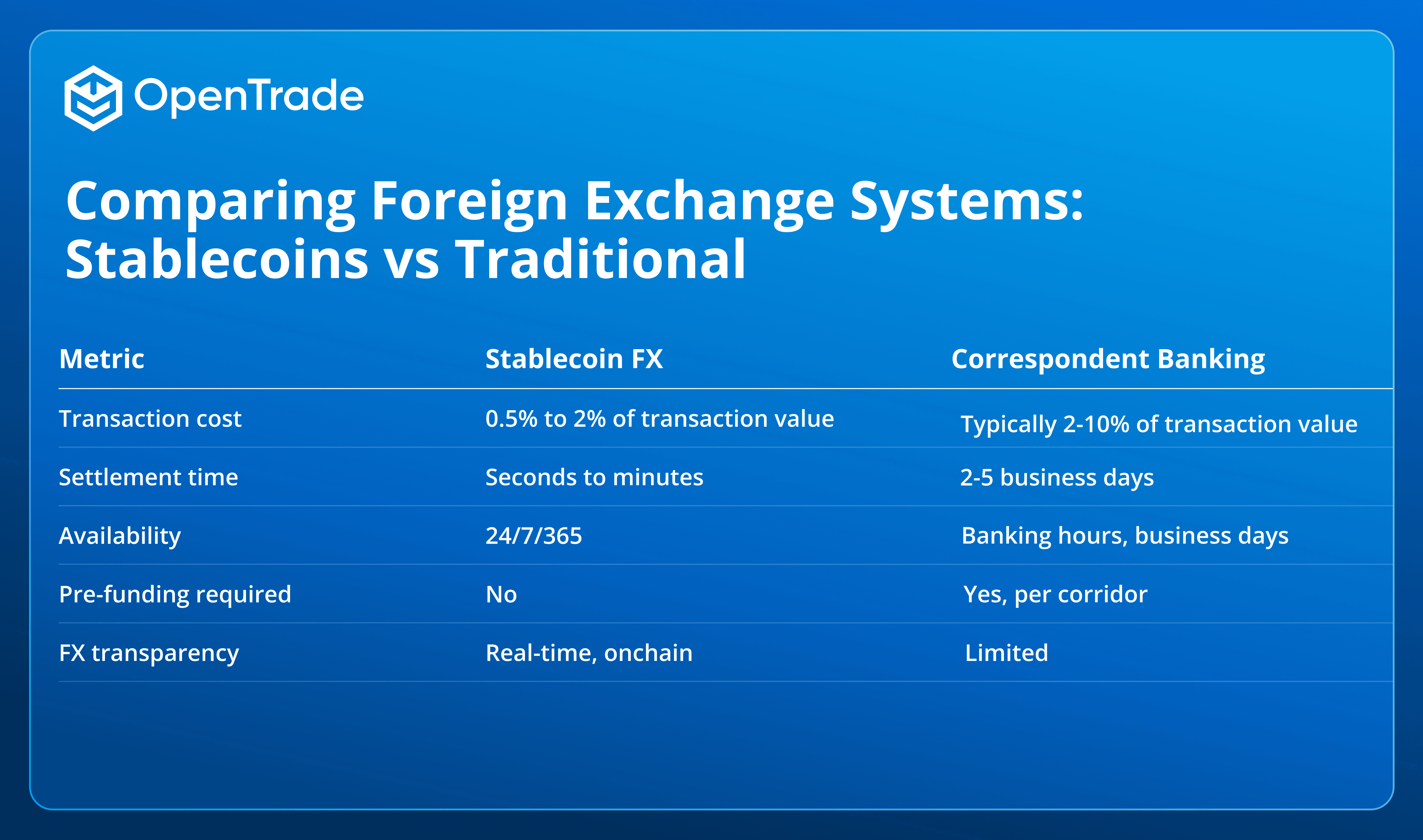

Comparing Traditional FX vs. Stablecoin FX

The gap between traditional and stablecoin FX across LATAM corridors comes down to four variables: cost, speed, availability, and capital efficiency. The table below breaks down how stablecoin FX compares to correspondent banking across the metrics that matter most to treasury teams.

Across B2B use cases, the total cost reduction from adopting stablecoins consistently lands in the 30-50% range when all cost components are included: transaction fees, FX spread, float, and intermediary deduction.

Which Exchanges Are Driving Stablecoin FX Adoption in LATAM in 2026

64% of LATAM's crypto activity takes place on centralized exchanges, with local platforms such as Bitso, Ripio, Mercado Bitcoin, Wenia, and SatoshiTango - becoming the primary access points, connecting stablecoin on-chain FX liquidity to local fiat rails, remittances, and B2B payments.

Exchanges running cross-border payment operations accumulate stablecoin balances as a natural part of their operations: float held between on-ramp and off-ramp settlement, reserves maintained for onchain FX liquidity, and treasury balances held between transaction cycles. On traditional banking infrastructure, that capital sits idle. On stablecoin yield infrastructure, capital is put to work.

Bitso is the most active exchange in onchain FX across LATAM. It processed over $6.5B in US-Mexico remittances in 2024 and serves 1,900+ enterprise clients across the region.

In 2025, Bitso Business launched FXaaS (Foreign Exchange as a Service), which lets institutional clients embed FX services directly into their own platforms, using Bitso's liquidity position and in-house trading desk for pricing across multiple LATAM currencies.

This is a direct move toward owning the FX infrastructure layer, not just being an exchange on top of it.

Founded in Argentina in 2013, Ripio is now operating across 7 countries, has shifted from a retail exchange to a B2B infrastructure provider, serving banks, fintechs, and enterprise platforms, including Mercado Libre.

Ripio CEO, Sebastián Serrano, described the coming decade as a "decade-long boom for stablecoins," and the company has repositioned around local currency stablecoins and tokenized assets to capture that shift.

Mercado Bitcoin is Brazil's largest exchange, partnered with Ripple in 2025 to expand its stablecoin settlement infrastructure. Brazil is the region's dominant market, with over 90% of Brazilian crypto flows now stablecoin-related, according to Chainalysis's 2025 Geography of Cryptocurrency Report.

These exchanges are not adapting to stablecoin FX as an afterthought. They are rebuilding their core payment infrastructure around it.

OpenTrade provides the infrastructure layer that connects exchange treasury to institutional-grade yield sources, including Fidelity and Franklin Templeton Money Market Funds, BlackRock ETFs, and private credit and trade finance assets, all managed by Five Sigma Finance, a UK-regulated asset manager overseeing $6B+ in AUM.

No on/off ramp required

No lock-ups

No transaction fees

Sub-30 days to launch

Idle capital stays on-platform, not flowing to competitors

Which exchanges are driving stablecoin adoption in LATAM in 2026?

Bitso, Ripio, and Mercado Bitcoin are three exchanges that are most actively building stablecoin FX infrastructure across the LATAM region.

Bitso leads the US-Mexico remittance corridor with $6.5B in 2024 volume and FXaaS for institutional clients. Ripio operates across seven countries and has repositioned as a B2B infrastructure provider. Mercado Bitcoin is Brazil's largest exchange and partnered with Ripple for stablecoin settlement expansion. For a broader look at the platforms driving adoption across the region, see OpenTrade's Stablecoin Surge LATAM report.

Are USD stablecoins or local fiat stablecoins better for the LATAM corporate treasury?

USD stablecoins are currently the preferred choice for cross-border B2B payments because they provide dollar-denominated value that protects against local currency depreciation, and they have by far the deepest liquidity across LATAM corridors.

Local currency stablecoins, including Ripio's wARS for the Argentine peso and Bitso's MXNB for the Mexican peso, are emerging for domestic transactions where the FX conversion step adds unnecessary cost. For corporate treasury, USD stablecoins remain the default for cross-border settlement, while local stablecoins are worth evaluating for high-volume domestic corridors.

Elena Beech