How Neobanks Can Offer a Fixed-Rate USD Savings Product in Under 30 Days with OpenTrade

Elena Beech

Key Takeaways

The APY on stablecoin yield products can be unstable, making it difficult to offer users a rate they can actually plan around. A rate that changes without warning can often be a source of user frustration and a potential retention risk.

Offering a fixed-rate product solves this. Users can see a clear, predictable return on their savings, plan their finances around it, and trust that the product will behave consistently over time. That predictability can make the savings product more sticky, especially to users who have a more conservative risk appetite.

For fintechs and neobanks, launching a fixed-rate product adds an additional revenue stream to the business: margin. Instead of passing the full yield generated through to the users, the platform takes a spread between what the underlying infrastructure generates and what the end user receives. That spread is a recurring revenue line that increases directly with the balance held on the platform.

However, building a fixed-rate USD savings product without an internal investment team has traditionally incurred significant time, capital, and human resources. With whitelabeled stablecoin yield infrastructure like OpenTrade, launching a new savings product takes under 30 days with a single API integration that seamlessly embeds into your existing user interface. This article explains how and what to look for when evaluating your options.

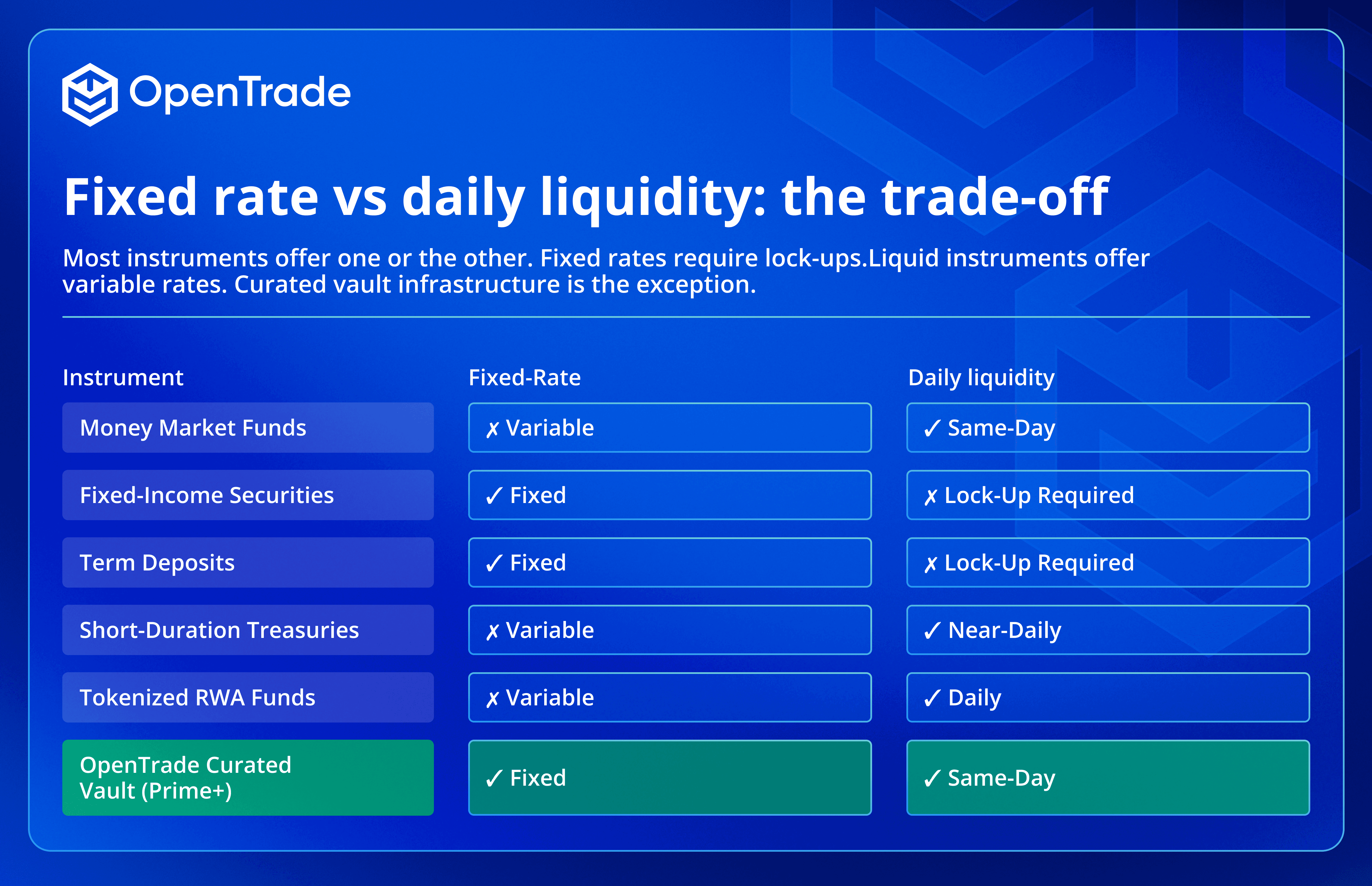

Fixed Rates vs. Daily Liquidity

Only about 15% of neobanks are profitable in 2026, and one of the most important factors for neobanks to be profitable is whether users stay on the platform, grow their balances, and engage with multiple different product types.

A competitive savings rate keeps users from moving money to a competitor. A fixed rate is often more attractive to users than a variable rate because they can plan around it. It shows up in the product as a set number they can trust rather than one that changes every quarter.

The problem is that a fixed rate creates an obligation. If a neobank promises users 4.5% per year on their USD balances and the underlying assets only deliver 3.8% in a given month, the difference comes out of the neobank's margin. Traditional financial instruments designed to manage this risk, such as interest rate swaps and structured notes, require a treasury team that understands them, a counterparty network that can price them, and enough balance sheet scale to make the cost worthwhile. For most neobanks, this means creating an internal investment team, which is time-consuming and costly.

There is also the liquidity side. Users of a savings product expect to be able to move their money. A neobank that locks users into 90-day terms to achieve a fixed rate will see lower adoption than one that offers the same rate with same-day or next-day withdrawals. Instruments that deliver fixed rates, such as fixed-income securities and term deposits, often require lock-ups. Instruments that offer daily liquidity, such as money market funds, typically offer variable rates. Getting both simultaneously is the key offering for users.

How Modern Fintech Yield Infrastructure Solves the Trade-Off

Two approaches have emerged for neobanks trying to resolve the fixed-rate versus daily-liquidity tension.

The first is tokenized RWA funds. These are digital representations of existing financial instruments, such as money market funds or Treasury ETFs, issued on a blockchain. The yield they generate reflects the underlying fund's performance, which means the rate varies with market conditions. Tokenized T-bill products were generating approximately 4-5% APY in Q1 2026. These products provide transparent, liquid access to institutional instruments, but they do not resolve the fixed-rate requirement. The user still sees a variable number.

The second is a curated yield vault structure, which is the model OpenTrade's fintech yield infrastructure uses. Here, the infrastructure provider manages a dynamically rebalanced portfolio of RWAs and blue-chip DeFi strategies, and uses that portfolio to deliver a fixed rate commitment to the neobank client on top of the variable underlying. Daily liquidity is maintained through allocation to short-duration, high-liquidity instruments, including commercial paper and money market funds, alongside reserves that can be accessed same-day or next business day.

The key operational distinction is who manages the rate exposure. In a tokenized RWA model, the neobank absorbs all of the market rate movements. For the curated vault model, the infrastructure provider actively manages the portfolio to deliver the agreed-upon fixed rate. For neobanks without a dedicated investment team, the second option is a quick and easy method to launch a fixed-rate USD savings product.

Evaluating the Source of High Stablecoin Yields in 2026

One of the most common questions is where high stablecoin yields actually come from, because the gap between what a U.S. bank pays on savings (approximately 0.05% to 3.5% APY on most accounts, with some high-yield accounts reaching ~4% APY) and what stablecoin yield products offer is large enough to raise legitimate questions.

The yield gap is stark, and it’s down to a combination of factors. Firstly, banks capture the spread between what they earn on assets and what they pay depositors, keeping the difference as their net interest margin. That margin funds their operations, capital requirements, and profit. Secondly, stablecoin yield infrastructure passes more of the underlying return directly to the product, with lower distribution costs and smaller intermediary margins.

The primary yield engines used to generate returns in 2026 include short-duration U.S. Treasuries and money market funds (~4% to 5% APR), investment-grade commercial paper (~4% to 6% APR), collateralized loan obligations and asset-backed securities (~5% to 7% APR), trade finance and private credit (~6% to 12% APR), and blue-chip DeFi lending protocols (~3.5% to 9% APR depending on utilization). A well-structured, curated vault blends multiple different yield sources across different durations and risk profiles, which is what allows a fixed rate commitment to be maintained even as individual source rates fluctuate.

Each of these asset classes carries a distinct risk profile.

Short-duration T-bills carry virtually no credit risk.

Commercial paper carries modest credit risk from the issuing institution.

Private credit carries higher credit risk in exchange for higher yield.

A fixed-rate product that delivers 4.5% APR from T-bills and commercial paper has a fundamentally different risk profile from one delivering 4.5% APR from private credit alone. Understanding the blend is the first thing any treasury team should ask for.

Risk Mitigation: What Institutional Buyers Look For

For a neobank evaluating a fintech yield infrastructure partner, there are four areas to assess before committing.

Custody and asset quality. Reserve assets should be custodied at Tier 1 Global Systemically Important Banks (GSIBs) or equivalent regulated custodians, not at the infrastructure provider directly. All real-world asset holdings should be rated investment-grade by third-party rating agencies. Ask for the specific custodian and rating on each underlying asset.

Reporting and transparency. Institutional-grade products publish reserve composition, daily NAV, and yield attribution. Weekly attestations from an independent, regulated asset manager are the minimum standard for a product that will sit on a neobank's balance sheet and be offered to users. If a provider cannot show you their reserve breakdown and attestation history, that is a material gap.

Speed to market and operational lift. For neobanks without internal investment teams, the entire value proposition of using infrastructure is that it reduces operational complexity rather than adding to it. An API-first integration that handles reserve management, reporting, and product configuration from a single endpoint is the benchmark. If onboarding requires the neobank to build bespoke infrastructure or manage multiple counterparties directly, the operational savings disappear.

OpenTrade's infrastructure meets all four of these criteria: bankruptcy-remote SPVs with reserve assets held at Tier 1 institutions, investment-grade asset selection managed by Five Sigma Finance (an FCA-regulated firm overseeing $6B+ in AUM), weekly attestations, and API-first integration. [INTERNAL LINK: opentrade.io/contact]

Build vs. Buy

The build-versus-buy decision for a fixed-rate USD savings product is more straightforward than it looks. Building in-house requires the neobank to establish relationships with asset managers, structure a legal vehicle for reserve segregation, build and maintain reporting infrastructure, and hire or contract investment professionals to manage rate exposure. The timeline is typically six to twelve months, and the operational cost is ongoing.

The buy model means integrating with a provider whose entire infrastructure stack is already built, regulated, and operational. The neobank's team connects via API, configures the product parameters, and launches.

OpenTrade's Prime+ Vault is the reference implementation of the buy model for a fixed-rate USD savings product. It is a Curation+ vault that delivers a fixed monthly APR targeted approximately 2% above the USD risk-free rate, with daily liquidity and no rate risk absorbed by the neobank. The underlying portfolio is actively managed to maintain the fixed-rate commitment across changing market conditions. There are no transaction fees, no lock-ups, and no on/off ramp required.

For neobanks that want a different fixed rate target, a specific risk profile, or a particular asset allocation, Curation+ allows those parameters to be configured around the client's requirements rather than a standard product. That flexibility is what makes the buy model work across different markets and user bases.

How do fixed stablecoin interest rates maintain daily liquidity?

A fixed-rate vault maintains daily liquidity by allocating a portion of the portfolio to short-duration, highly liquid instruments, including commercial paper, money market funds, and blue-chip DeFi lending protocols that allow same-day redemption. The fixed rate is maintained across the full portfolio, not just the liquid portion.

The infrastructure provider actively manages the allocation to ensure enough liquidity is available to meet expected redemption requests while the higher-yielding assets continue to accrue. For the neobank, this means users can withdraw funds on a same-day or next-day basis without the neobank needing to manage the underlying liquidity itself.

How is the fixed rate maintained if global interest rates fluctuate?

A fixed-rate product targeting approximately 2% above the risk-free rate is structured to adjust with market conditions rather than fix against an absolute number. If the U.S. federal funds rate moves materially, the target rate adjusts alongside it. The "fixed" element is the spread above the benchmark, not the absolute APR.

The infrastructure provider manages the portfolio to maintain that spread through active rebalancing: when T-bill yields compress, allocation shifts toward higher-yielding instruments within the approved risk parameters. The neobank's obligation to users is communicated as an expected rate range rather than a guaranteed absolute figure, which both reflects the underlying economics and protects the neobank from margin risk. All yields are variable, and past performance is not indicative of future results.

Can a fintech use the same infrastructure for corporate treasury management and user-facing yield payout?

Yes, OpenTrade's infrastructure can be used for both use cases through the same API integration. A neobank can use the platform to earn yield on its own stablecoin treasury balances (operational float, reserve capital etc) while also powering a user-facing savings product at the same time. This means a single integration covers the internal treasury opportunity and the product opportunity simultaneously, rather than requiring two separate vendor relationships.

Elena Beech