How to Evaluate Stablecoin Yield Risks: A Guide for Fintechs

Elena Beech

Key Takeaways

With stablecoin market capitalization surpassing $310 billion in 2026, fintechs are looking for stablecoin yield products that offer institutional-grade risk-adjusted returns that can offer their users with confidence.

The potential risks of stablecoin yield products are real, specific, and often underestimated. Depegs and volatility get most of the attention, but for fintechs operating at scale, the more pressing stablecoin yield risks sit in the operational, legal, and structural layers underneath, such as counterparty concentration, liquidity constraints, reserve quality, yield source, and sustainability.

This article breaks down the five stablecoin yield risks that matter most to fintech CFOs, CTOs, and product teams, and what to evaluate before integrating yield infrastructure into your platform.

What Stablecoin Yield Risks Matter Most to Fintechs?

Most articles on stablecoin risk management focuses on retail investors worrying about whether a coin will hold its dollar peg. For fintechs integrating yield infrastructure into real products, there are many other factors to consider. A fintech offering a yield-bearing dollar account to millions of users carries a completely different risk surface than an individual holding tokens in a personal wallet.

The five risks below represent the operational and structural challenges that practitioner discussions, treasury forums, and institutional due diligence processes consistently surface as the ones that matter most at scale.

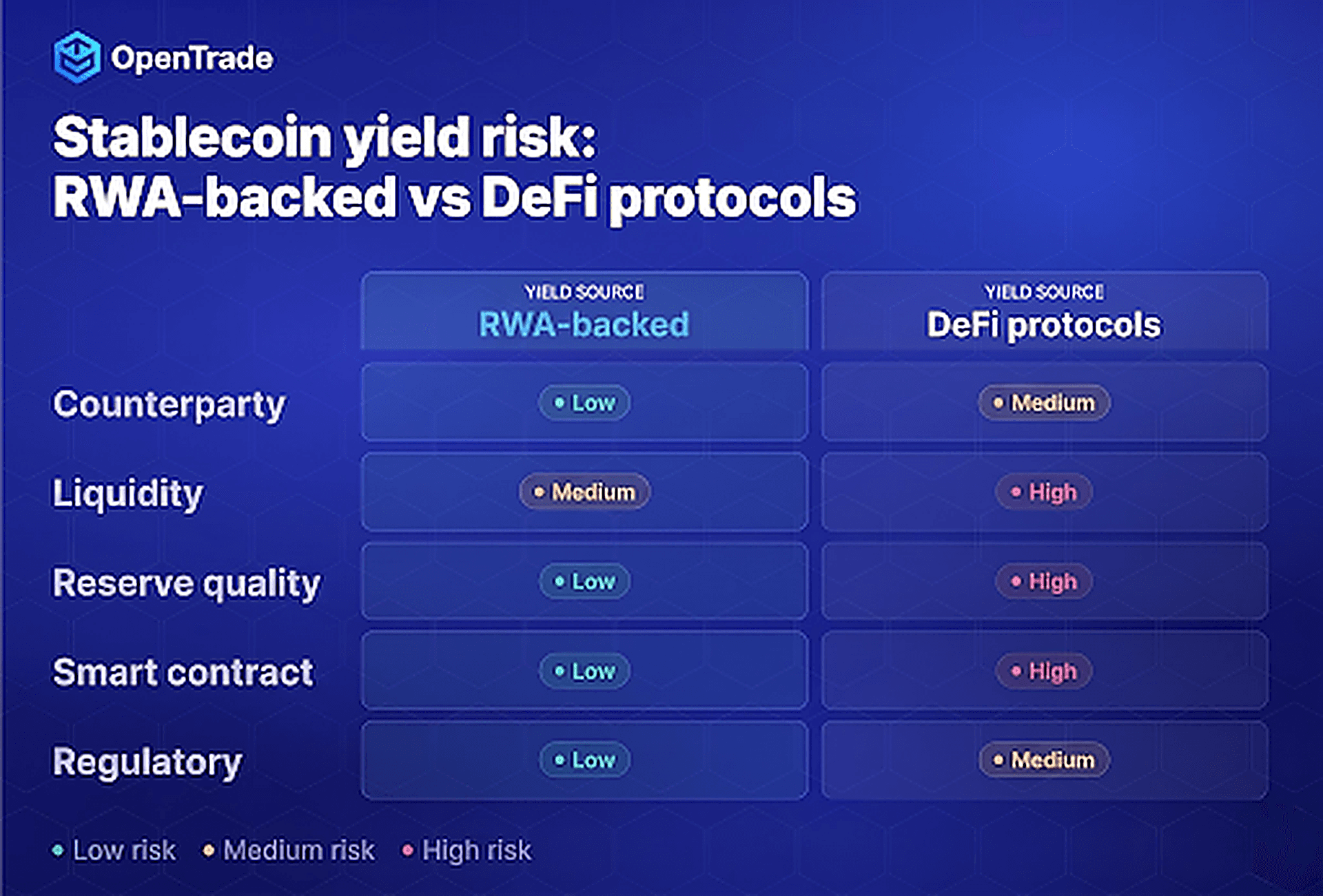

1. Counterparty Risk: Who Is Actually Holding the Assets?

Counterparty risk is the most underrated stablecoin yield risk for fintechs, and one of the most important. What happens to the assets backing your yield product if an intermediary fails, freezes withdrawals, or restructures?

The structural exposure varies significantly depending on how yield is generated. Real-world asset (RWA) vault products backed by U.S. Treasury bills or money market funds route through a chain of counterparties, including issuers, custodians, and asset managers. DeFi lending protocols like Aave introduce smart contract risk and protocol governance risk. Centralized earn programs carry platform insolvency risk, as the collapses of Celsius and BlockFi clearly demonstrated.

For fintechs, the key due diligence questions are:

Who holds the underlying assets?

Under what legal structure are they held?

What protections exist if that entity fails?

Bankruptcy-remote special purpose vehicles (SPVs) with independently held collateral provide materially stronger protections than commingled custody arrangements. Without that legal separation, a counterparty failure can leave your users' funds frozen in insolvency proceedings rather than redeemable on demand.

A UK-regulated asset management firm like Five Sigma Finance, which manages assets on behalf of OpenTrade, provides a substantially different risk profile than an unregulated DeFi protocol or an offshore earn program. That means a platform investing through OpenTrade has a named, regulated counterparty behind every transaction, weekly attestations confirming what's held and where, and a fully perfected security interest on every asset at every stage. An unregulated DeFi protocol or offshore earn program offers none of that. If something goes wrong, there's a legal structure to fall back on.

2. Liquidity Risk: Can Your Users Actually Get Their Money Out?

Stablecoin yield products are often marketed and adopted based on headline APR figures. When, how, and under what conditions users can withdraw their money receive far less attention. For fintechs managing user expectations and operational cash flow, this is a significant stablecoin yield risk.

The practical concern is exit liquidity under stress. DeFi money markets and synthetic dollar strategies can seize up during periods of volatility, when multiple parties attempt to exit simultaneously. Withdrawal queues, exit fees, and temporary freezes have occurred across multiple platforms. For a CFO, that's not an abstract risk.

If users can't access funds when they expect to, customer support volume spikes and the brand takes the reputational hit regardless of where the fault lies. Churned users are expensive to replace, and a liquidity incident raises acquisition costs while compressing LTV at exactly the wrong moment, disrupting operational cash flow.

For fintechs integrating yield infrastructure, the relevant questions are:

What are the withdrawal timelines under normal conditions and under stress?

Is there a maximum settlement window?

Does the platform provide transparency on liquidity depth?

Best-practice infrastructure processes withdrawals on a best-efforts T+0 / T+1 basis, with a maximum settlement period clearly defined.

Fintechs should also consider how withdrawal terms interact with how their own products are designed. A consumer-facing savings product that promises instant access creates a liquidity mismatch if the underlying yield infrastructure requires multi-day settlement. That gap needs to be managed explicitly, not just assumed.

3. Reserve Quality and Yield Source Sustainability

Not all stablecoin yield is created equal, and understanding where the yield comes from is central to stablecoin risk management.

Yield backed by short-duration U.S. Treasury bills and investment-grade money market funds reflects actual economic activity and carries predictable, auditable risk characteristics.

Yield generated from DeFi lending protocols fluctuates with borrowing demand. For example, Aave's USDC rate sat at approximately 3.94% on June 1st 2026, then compressed to below 1.5% within two weeks as borrowing demand fell. That kind of volatility makes DeFi lending unreliable as a treasury tool. In contrast, the USD risk-free rate moves gradually and predictably, tied to central bank policy rather than on-chain utilization.

Synthetic strategies like delta-neutral staking can deliver 4-15% APY but introduce funding rate risk that can unwind sharply and without warning.

For fintechs, reserve quality affects both risk and user experience. A product built on RWA-backed yield infrastructure delivers more predictable returns with a stronger risk framework than one dependent on DeFi funding rates. Platforms that provide weekly attestations from regulated asset managers, legally binding loan confirmations for every deposit, and real-time transparency into collateral holdings offer a substantially stronger due diligence foundation than protocols with opaque or infrequently audited reserve structures.

Stablecoins are projected to grow to $0.5-$3.7 trillion by 2030. As the market scales, reserve quality differentiation will become a more significant driver of institutional preference.

4. Smart Contract and Infrastructure Risk

For fintechs generating yield through on-chain infrastructure, smart contract risk is another factor that should be considered. Smart contract exploits and protocol vulnerabilities have resulted in significant losses across the DeFi ecosystem, and the risk is not eliminated by audit history alone.

The StablR exploit in May 2026, which saw $8.35 million minted against zero collateral through a multisig flaw, is a clear demonstration of how infrastructure vulnerabilities can bypass economic security assumptions entirely. The exploit did not require a counterparty failure, it only required a technical flaw in access controls.

For fintechs evaluating yield infrastructure, the relevant questions include:

What is the audit history of the underlying smart contracts?

What access controls govern protocol upgrades and administrative functions, and what insurance or backstop mechanisms exist in the event of a protocol failure?

Platforms that operate through legally binding agreements with custody controls, asset segregation, and known counterparties carry a fundamentally different technical risk profile than permissionless protocols.

The distinction between institutional-grade yield infrastructure and DeFi yield aggregation matters here. Fintechs serving regulated markets need infrastructure with a security model they can explain to their own compliance and legal teams, not just to their technical team.

How OpenTrade Addresses These Risks

OpenTrade provides institutional-grade stablecoin yield infrastructure designed specifically for fintechs. Each vault operates through a bankruptcy-remote SPV with independently held collateral, weekly attestations from Five Sigma Finance, a UK-regulated asset management firm managing over $6B for institutional clients, and legally binding loan confirmations for every deposit.

Yield sources include Fidelity and Franklin Templeton Money Market Funds, BlackRock High Yield Corporate Bond ETFs, and private credit and trade finance assets: all fully backed by real-world assets, generating approximately 2-10% APR on stablecoin balances.

Fintechs integrate via a single API in under 30 days, with no requirement to build underlying infrastructure from scratch. Withdrawals are processed on a best-efforts T+0 / T+1 basis, with a maximum settlement period of two business days.

Get in touch to discuss yield infrastructure for your platform

What is a safe stablecoin yield?

There is no universally accepted definition of "safe" stablecoin yield, but the characteristics that distinguish lower-risk yield infrastructure from higher-risk alternatives are well established. Yield backed by short-duration U.S. Treasury bills and investment-grade money market funds carries more predictable risk characteristics than yield generated from DeFi lending protocols or synthetic derivative strategies.

The safest yield structures for fintechs are those that operate through bankruptcy-remote legal entities, with independently held collateral, regulated asset management oversight, and clearly defined withdrawal mechanics.

Why are stablecoin yields so high?

Stablecoin yields vary significantly depending on the source. Yields backed by U.S. Treasury bills reflect the USD risk-free rate, currently in the 4-5% range. Yields from DeFi lending protocols fluctuate with borrowing demand and can spike during periods of high market activity. Yields from synthetic strategies like delta-neutral staking reflect funding rate dynamics and can be significantly higher but also far more volatile.

Higher yields almost always reflect higher risk, higher counterparty exposure, more complex exit mechanics, or greater sensitivity to market conditions. Fintechs should evaluate yield sources carefully rather than optimizing purely for headline APR.

Elena Beech